I recently read an article on the dilemma employees face when they are offered a choice of investing in a traditional 401(k) or a Roth 401(k). Like many things in life, this feels like it should be a simple decision, but clearly there’s no right answer, otherwise employers would only offer one plan or the other. For all of the examples to follow, we’ll imagine four workers are starting jobs with drastically different salaries of $35,000, $75,000, $100,000, and $120,000 a year. We’ll imagine they’re all serious about retiring, and can invest 15% of their income before taxes ($5,250, $11,250, $15,000, and $18,000). We’ll assume each receives a 100% company match on their first 5% of contributions ($1,750, $3,750, $5,000, and $6,000). As usual, we’ll assume a 7% rate of return.

When most people calculate the amount they can invest into a 401(k) (Roth or traditional), they use similar assumptions as I did. But in reality, I don’t know of anyone who budgets this way. Most people have a combination of fixed and variable expenses, and choose the amount to invest based on their “surplus.” If you have a budget you can quickly see how much money you have to invest. The reason I make this distinction is because your take-home pay varies based on if you invest in pre-tax or after-tax investments. This is why 401(k) plans are so appealing in the first place.

People earning $35,000 and investing 15% of pre-taxed income will invest $202 every two weeks, but their paycheck will only be reduced by $138. This chart shows the amount invested and the amount the paycheck is reduced.

| Salary | $35,000 | $75,000 | $100,000 | $120,000 |

| Invested bi-weekly | $202 | $433 | $577 | $692 |

| Take home pay reduction | $138 | $265 | $357 | $404 |

| Difference | $63 | $168 | $220 | $288 |

| Invested annually | $5,250 | $11,250 | $15,000 | $18,000 |

| Annual take home pay reduction | $3,599 | $6,878 | $9,278 | $10,503 |

| Annual difference | $1,651 | $4,372 | $5,722 | $7,497 |

As you can see, the difference between what is invested in a traditional 401(k) and the amount take-home pay is reduced by is significant. I used ADP’s payroll calculator to estimate what taxes would be for each income bracket (single worker, living in Connecticut). In each scenario, investors take home around 5% more of their income by investing in a traditional 401(k) instead of a Roth 401(k).

So the issue is, we stated each person would invest 15% of their salary, but in reality, while 15% of their income is going into the 401(k) account, the investor’s paycheck is only be reduced by around 10% if they invest in a traditional 401(k). This creates an apples to oranges comparison of traditional and Roth 401(k) plans. If we say each person has the same take home pay no matter which plan they use, then the contribution amounts change drastically. To create an apples to apples comparison, we’ll ensure the take-home pay remains the same no matter which 401(k) plan is used.

| Salary | $35,000 | $75,000 | $100,000 | $120,000 |

| Take-home pay in either scenario | $22,479 | $42,169 | $53,882 | $62,583 |

| Amount invested in Roth 401(k) | $5,250 | $11,250 | $15,000 | $18,000 |

| Percent invested in Roth 401(k) | 15% | 15% | 15% | 15% |

| Roth 401(k) company match | $1,750 | $3,750 | $5,000 | $6,000 |

| Combined annual contribution | $7,000 | $15,000 | $20,000 | $24,000 |

| Amount invested in trad. 401(k) | $7,650 | $18,000 | $18,000 | $18,000 |

| After-tax contribution | $0 | $257 | $3,867 | $7,497 |

| Percent invested in trad. 401(k) | 22% | 24% | 22% | 21% |

| Trad. 401(k) match | $1,750 | $3,750 | $5,000 | $6,000 |

| Combined annual contribution | $9,400 | $22,007 | $26,867 | $31,497 |

As you can see from the chart, by investing in a traditional 401(k), depending on your salary, you can invest 6% to 9% more money while taking home the same amount as if you invested 15% of your salary in a Roth 401(k). At an income of $75,000 and above the calculations get a little more complicated because you will be investing beyond the $18,000 tax free limit, after which all contributions are taxed at your effective tax rate.

With this information you now can make a more informed opinion on how to invest your money. Assuming you work 30 years without a raise, earning an average return of 7%, here’s how much money you’d have with each scenario.

As you can see, the more you make, the greater the impact from investing in a traditional 401(k) is to your ending 401(k) balance (25.5%, 31.8%, 25.6%, and 23.8% higher ending balance). The debate then isn’t about which account will leave you with a higher account balance, but rather which one will provide you with more money at retirement.

When you withdraw your money from a Roth 401(k) you don’t pay any taxes on the amount you contributed, or the earnings on your contribution. You do pay taxes on the amount your employer contributes, as well as the earnings on your employer’s contributions. When you withdraw your money from a traditional 401(k) you pay taxes on the amount you contributed, and the earnings on your contribution. You also pay taxes on the amount your employer contributes, as well as the earnings on your employer’s contribution. You do not pay taxes on any after-tax contributions you made, but you do pay taxes on the earnings from your after-tax contributions. Confusing yet?

To calculate the taxes on each account, we’ll assume the only retirement income you’ll have is from your 401(k), and that you’ll live 25 years after you retire. To make the calculations easier, we’ll also assume you move the entire balance of your 401(k) into cash, earning no interest.

| Amount to withdraw each year | ||||

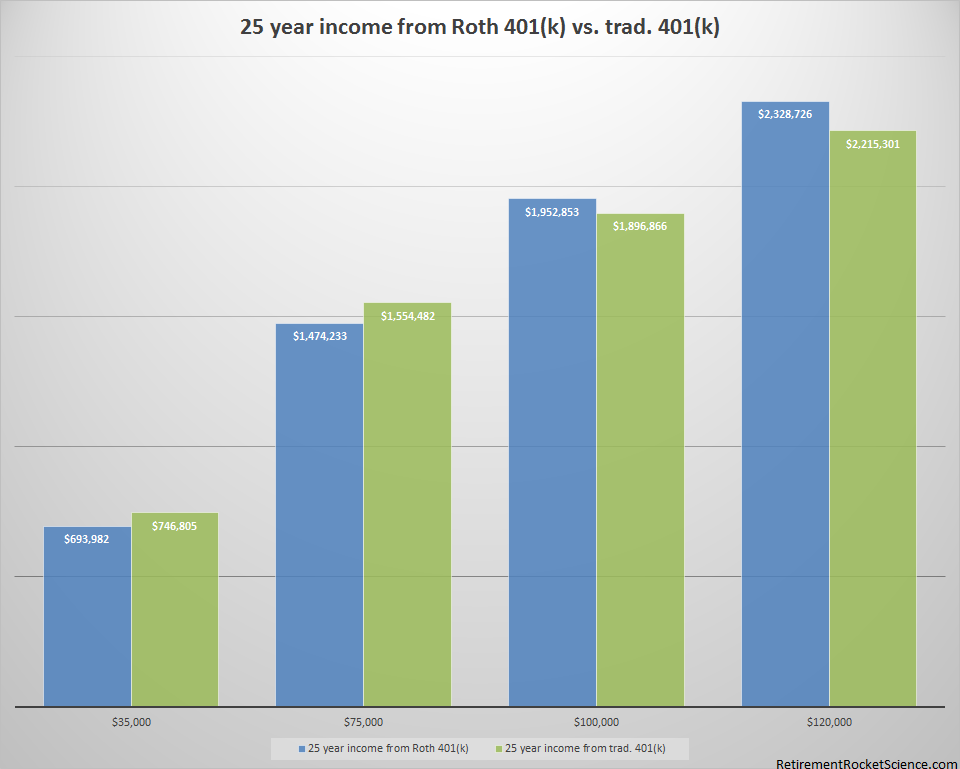

| Old salary | $35,000 | $75,000 | $100,000 | $120,000 |

| Roth 401(k) income | $27,759 | $58,969 | $78,114 | $93,149 |

| Trad. 401(k) income | $29,872 | $62,179 | $75,875 | $88,612 |

| Annual difference | -$2,113 | -$3,210 | $2,239 | $4,537 |

| 25 year difference | -$52,823 | -$80,249 | $55,987 | $113,425 |

| Advantage | Traditional 401(k) | Traditional 401(k) | Roth 401(k) | Roth 401(k) |

| As a % of account balance | 7.5% | 5.3% | 2.1% | 3.6% |

As you can see, if you make $35,000 a year, you’re much better off investing in a traditional 401(k). The reason for this is you have more money working for you over a longer period of time. As you start to make more money, the Roth 401(k) becomes the better choice. The reason for this is less impact from taxes. What is interesting though is for the majority of workers, making the wrong choice here isn’t as big of a deal as you might think.

This is one decision I wouldn’t lose sleep over. As you start to have more taxable income in retirement, the Roth 401(k) becomes a better option. But no one has a crystal ball to know what tax rates will look like for retirees in the future. The real winner is the people who start to save early, no matter which type of account they invest in.

If you have any questions or comments, you can reach out below or continue the discussion in the forum. If you are interested in receiving a notification of new posts, you can subscribe here.