Folks become landlords for many reasons, but whatever the reasons, it’s important to have an objective with a rental property. Some people might want to buy a place today in a location they intend to retire to, and will use the rental income to help pay off the mortgage. Others might be waiting for property values to increase before selling a house that’s currently worth less than the mortgage. Perhaps the rental is a form of investment diversification, or maybe you want some sort of active participation in your investment. Whether intentional or accidental, the goal of every landlord should minimally be to not lose money!

Just as it rarely makes sense to pay down a mortgage on a primary residence, as you pay down the mortgage on a rental property the equation behind the profitability of holding onto the rental might change. How so, you might ask? Imagine you bought a house worth $200,000, putting 20% down ($40,000), with an interest rate of 4%. Your monthly mortgage payment would be $764 a month, and we’ll assume another $336 a month in taxes, for a total payment of $1,100. If you can rent the property out for $1,500 a month, during the first year you’d take in $18,000, with $6,350 going towards interest, $2,820 towards principal, $4,030 towards taxes, $800 towards insurance, and $4,000 going in your pocket. In a way, it’s like making $6,820, as you’ll hopefully recover the money applied to the principal.

Either way you look at it ($4,000 or $6,820 before taxes), you’re doing pretty well on your $40,000 investment (10% or 17% return). Of course, this is a best case scenario. There are plenty of landlord horror stories, and even with the greatest tenants in the world there are going to be months your rental sits vacant, carpet that needs to be replaced, walls that need to be repainted, roofs to be re-shingled, and all of the other joys that come with home ownership. A common suggestion is to set aside 2% of the property value each year towards these expenses, which in our example would be $4,000 for the first year. This isn’t to say you’ll actually spend 2% a year, but whenever you need to replace a furnace or have to install new windows, you’ll be glad you set some money aside. I’m interested to see what typical percentages other landlords spend; feel free to comment below or in the forum.

Setting aside $4,000 a year changes the investment return a bit, to $0 or $2,820 (excluding or including principal reduction) a year (0% to 7%). I’d be pretty happy with a 7% return, and depending on your reasons for being a landlord, you might be okay with 0%. After all, the money in your pocket today isn’t everything; you might make money in other ways too, such as tax deductions and ultimately when you go to sell the property.

Imagine you rent this house out for 15 years. Here’s where the numbers change a bit. We’ll assume you increase the rent by 2% each year, and property taxes increase 2% each year as well. 15 years from now you’ll be paying $5,130 a year towards principal, $4,040 in interest, $1,000 for insurance, and $5,320 in taxes, for a total of $15,500. You’d be pulling in $23,750 a year in rent, leaving you with $8,250 a year in your pocket. Combine that with the amount put towards principal, and you’re looking at $13,380. From your $40,000 investment you’re now looking at a return of 20% to 33% a year.

If you take a step back, 15 years later you’d owe $103,200 on the house. If house values didn’t increase, you’d have $96,800 in equity, and if house values increased 1% annually, you’d have $129,000 in equity. Imagine you sold the house at this point. After taxes, commissions, and fees, you might walk away with $103,500. If you had been saving your profit over the past 15 years and investing it at a 7% rate, you’d have an additional $26,600, for a total of $131,000. If you invested this amount for 15 more years, you’d have an ending balance of $309,700 after taxes with a 7% return.

On the flip side, if you kept the house for all 30 years, you’d have a house worth $270,000, and an investment from the rental profits worth $172,100, for a total of $441,600. Once you sell the house though, you’ll have to pay taxes and fees. If you sold the house after 30 years, you might pocket a total of $407,400 for all of your efforts. If you sold after 15 years you’d have made an average annual return of 7.06% on your investment, if you sold after 30 you’d have averaged an 8.04% annual return. For an extra .98% return, does it make sense to hold onto an investment that requires more of your time as it ages? Then again, perhaps you feel returns from a rental have a greater chance for being more stable than the general market.

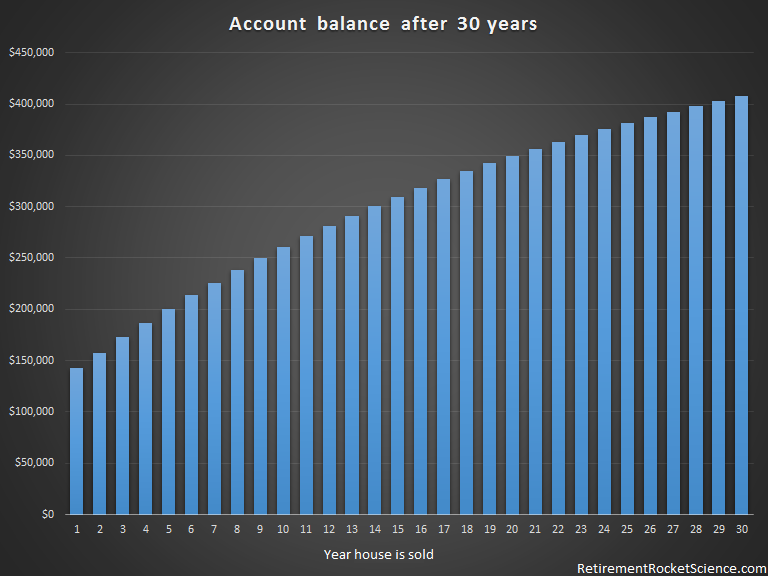

Each year you hold onto the rental the amount of money you’d gain from selling the property and investing all of the proceeds decreases. It’s important to note that the number is still positive, but only you can determine if that amount is worth the effort you’re putting into your property. The first chart shows how much money you’d have if you sold the property and invested the proceeds for the remaining years. So the first bar assumes you sold the house after 1 year of ownership and invested the money for 29 more years, and the last bar assumes you sold the house after 30 years and invested the money for 0 years.

The second chart shows the additional amount of money your investment would be worth by waiting a year to sell. So by selling the house after owning it for 2 years instead of 1 you’d make an additional $15,400, whereas if you sold it after owning it for 30 years instead of year 29 you’d make an additional $4,700.

Every rental is different, but the point here is to make sure that every so often you reevaluate your situation. What made sense 5 or 10 years ago might not make sense today. If you see a few major repairs coming up on the horizon, maybe it makes sense to sell the rental and put the money to work somewhere else, perhaps even another rental. Part of what makes a rental profitable is you can use someone else’s money to generate income. This goes back to my original point about why it might not make sense to prepay your mortgage. The same numbers work here too. Even still, you might have to rent a house for 6 years before you’d do better than you would just investing the money.

Imagine you paid $200,000 cash for your rental. At the end of 30 years, your invested rental income plus the value of the house could be $1,012,500. If you sold the house, after taxes and fees you’d have $978,200. Not too shabby! Despite how big those numbers look, it’s only a 5.43% annualized return, compared to an 8.04% by taking out a mortgage ($200,000 outlay for $978,200 compared to a $40,000 outlay for $407,400). If you invested $40,000 at 7% you would be looking at $226,500 after 30 years assuming you invested the money in a taxable account, and $1,132,500 if you invested $200,000 at 7%. As you can see, if you only have $40,000, you’d do better buying the $200,000 rental, but if you had $200,000, you’d do better investing the $200,000 versus using it all to buy a rental. Of course, things aren’t always black and white. If you had $200,000 you could use $40,000 to buy a rental and invest the other $160,000. Then you’d have an ending balance of $1,301,300, or an annualized return of 6.4%. And if all rentals were predictable with great returns, everyone would invest in real estate and the stock market would be mighty lonely.

From this example, if I had $200,000 in cash lying around, I’d think long and hard before purchasing an investment property outright. It would make much more sense to pick up 5 properties with that amount of money. 30 years later you could have turned $200,000 into $2,037,000.

There are too many variables to say if becoming a landlord is a good investment strategy for you. It’s important to realize that as time goes on, those variables change. The tax savings from paying interest disappear when the loan is paid off, and without refinancing or selling, equity is trapped inside the rental, unable to earn a higher return that’s available elsewhere.

If you’re deciding whether enter or leave the world of rental properties, just realize that whichever decision you make, investing in a rental or investing in the market, you’re better off than the millions of other people doing neither. Which would you lose more sleep over, paying the mortgage on a rental that has been vacant for 3 months, or your retirement account going from $750,000 to $600,000 during a downturn in the market? Picking the wrong tenant or picking the wrong investment? Unlike many financial topics, all you can do is make a best guess, and realize there might not be a wrong answer.

If you have any questions or comments, you can reach out below or continue the discussion in the forum. If you are interested in receiving a notification of new posts, you can subscribe here.

Permalink

Very well done, Mark. Oh to be young again and realize that some day I shall be old. Hardest thing in the world for most young people to realize. When I was 25, I honestly could not picture being 40, At 45, I honestly could not picture being 65. Here I am at 76 1/2, and some days have difficulty picture being 77. So, what will I be thinking, if God lets me see 82+?