Much of the financial advice concerning retirement planning out there focuses on how to invest in a 401(k). There are a couple of reasons for this; the biggest being that more than 23% of workers actively participate in their company’s 401(k) plan, with the most participants of any company sponsored plan. Another is because employees with access to a good 401(k) plan typically earn more money than workers without access to any defined contribution plan, including 403(b)s, 457s, and Thrift Savings Plans: retirement plans were only available to 31% of low-wage public sector employees, compared to availability of 88% to high-wage employees. But none of these reasons why advice focuses on 401(k) plans really matter if you work in an organization that doesn’t offer employees a 401(k) plan.

The 401(k) is the best-known member of the defined contribution plan family, with over 52 million participants holding $4.7 trillion in 2015. The other members of that family include the 403(b), which are for employees working in public education and most nonprofit organizations. About 6.3 million participants have around $872 billion invested in their 403(b) plans.

457 plans are for state and municipal employees, as well as employees of qualified nonprofits. They can be offered along with a 403(b), and participants held around $266 billion in these accounts. Thrift Savings Plans (TSPs) are for federal employees. In 2015, there were around 4.6 million participants with $441 billion invested.

As you can see, the 401(k) has the most number of participants, along with the largest piece of the retirement savings pie. Many defined contribution plans operate under the same rules, so if you participate in a plan other than a 401(k), you can usually just substitute your plan’s nickname when reading financial advice.

But what about the other 86,464,000 million employed folks who aren’t participating in any employee sponsored plan? The Bureau of Labor Statistics reported that 66% of workers have access to a retirement plan at work, which means about 12 million people choose not to participate in a plan offered to them, while about 75 million have no employer-provided plan.

There are a few reasons why folks might not contribute to work sponsored plan, including not being eligible for one reason or another. But I’d wager the primary reason is because of a perceived lack of money to contribute, though a perfectly valid reason is because the plan offered by the employer just plain sucks.

If your plan doesn’t offer any sort of match and has high fees, you might be better off investing with the folks who don’t have access to any workplace plan. Just what should those folks be investing in?

In a previous post I discussed how someone should spend his or her paycheck. Then came the question of if someone with a good 401(k) should invest beyond the company max.

In general, a good course of action for most people is to:

- Contribute as much as it takes to get your company match in your 401(k)

- If you’re under the income limits, max out a Roth IRA

- Contribute to your 401(k) until you reach the tax deferred limit ($18,000 in 2015)

- Invest money in a brokerage account

- Invest after-tax money into your 401(k)

If steps 1, 3 and 5 aren’t options, starting with step 2 is probably a good starting point, but a lot of it comes down to taxes. Once again, you’re forced to pull out your crystal ball, which means a hybrid strategy might be the best course of action.

Why do you need to be a psychic? Imagine 2 people who earn $50,000 a year, where one has a 401(k) that doesn’t offer a company match, and the other works at a company that doesn’t offer any retirement plan. The first worker decides to put away 5% of his salary, or $2,500 a year. Since that’s pre-tax, the total taxable income is $47,500. His tax federal tax liability will be around $4,519, meaning he’ll take home $42,981.

Person 2 will have a tax liability of $4,894, meaning he’ll take home $45,106. That’s a difference of $2,125. If he invests that into a Roth IRA, he’ll be investing $375 less a year than person 1.

If both people invest these amounts for 30 years at the usual 7%, person 1 (no company match) will have an ending account balance of $252,682.60, and person 2 (Roth IRA) will have $214,780.21. That seems like a no-brainer, right? Invest in the no-match 401(k) and you’ll have $37,902.39 more at retirement.

Of course, nothing is ever that easy. You see, you’ll owe taxes on the money you pull out of your 401(k), and you’re taxed at ordinary income rates. This is where the crystal ball comes in. If you’re in the 25% tax bracket come retirement, after taxes you’d have $189,511.95, whereas you pay no taxes on your Roth IRA withdraws.

If you really retire with a $250k nest egg though, you’ll probably pay next to nothing in taxes because you’ll most likely be near the poverty line. Retire with a $2.5 million 401(k) balance and you can be sure you’ll be paying a good amount of taxes, making the Roth IRA all that more attractive.

So after investing in an IRA of some type, or both types, up to the limit, then what? Or what if your company’s retirement plan fees are sky-high? In this case, you’re on your own to invest by opening a brokerage account. It might sound scary, but it’s very easy to do. The options out there are well beyond the scope of this article, but companies like Fidelity and Vanguard are well-known for offering some of the lowest fees in the industry. In fact, many plans offered by employers offer funds by both of these institutions.

Because of the low fees these companies charge, it often makes sense to investigate investing in them if the funds offered by your company’s plan charge high fees. You’ll have to read the fine print to know, but it is well worth the effort.

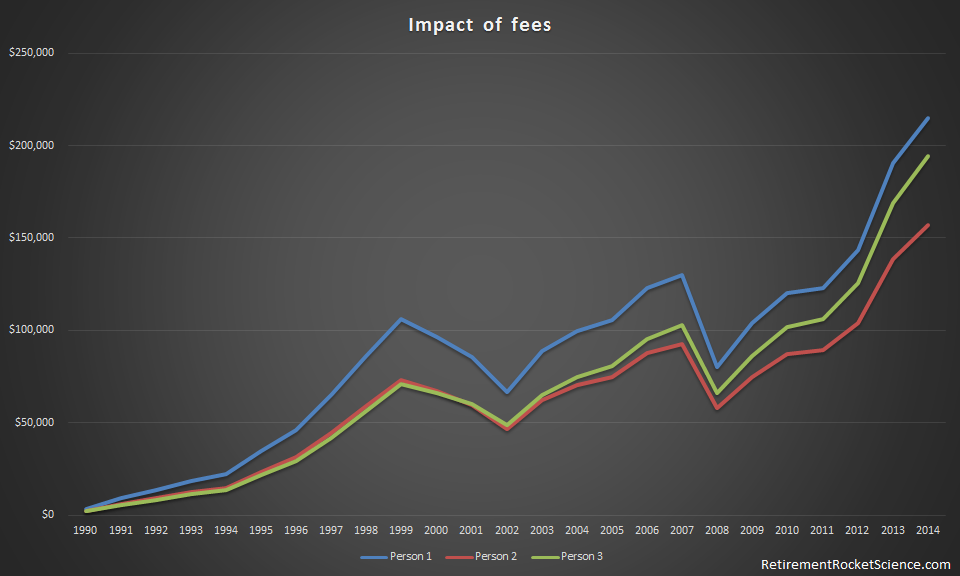

Fees can really add up. We’ll imagine 3 people. The first works at a company that charges a relatively high 401(k) fee of 3%, and offers a 50% match on up to 5% of your total contribution. The second works at a company charging a slightly lower fee of 2.4%, but the company offers no match. The third person doesn’t have a 401(k) at work, and invests his money in VOO, the Vanguard S&P 500 ETF.

All make $50,000 a year, with the first 2 contributing 5% of their salary a year ($2,500). We’ll assume they are in the 25% tax bracket, and take home $45,106. The third person contributes to a Roth IRA using after-tax money. If he has the same $45,106 take home, that gives him $2,125 a year to invest.

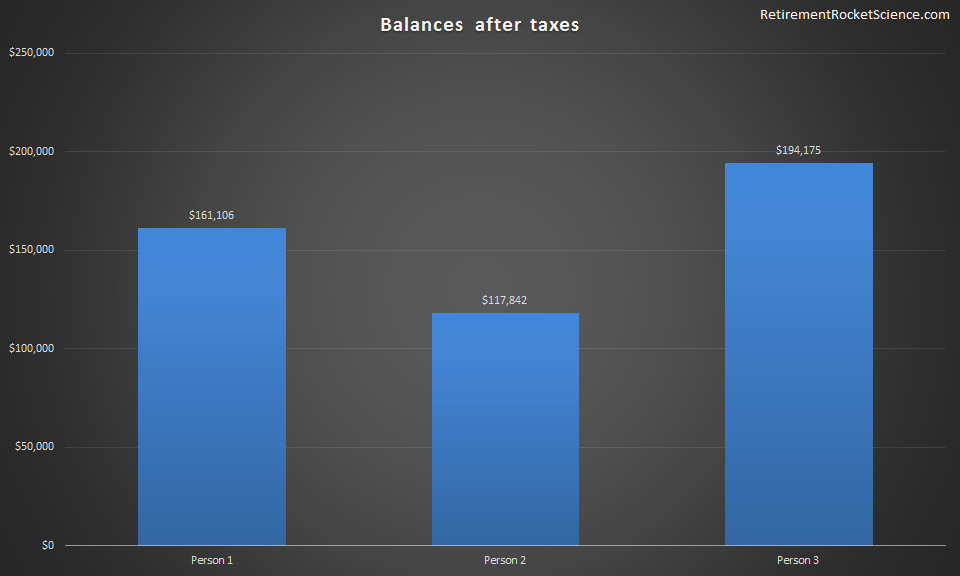

Imagine each person invested from 1990 until 2014, or 25 years. Using actual market returns for these years, here’s where they’d end up. Person 1 would have $214,808, person 2 would have $157,123, and person 3 would have $194,175.

As you can see, those fees are killer. If person 1 paid the same fees as person 3, they would have an ending account balance of $342,662, a 59.5% larger ending balance.

The 401(k) plans look even worse come retirement. If you’re in the 25% tax bracket, your ending balances will look more like the following chart.

As you can see, even with an employer match, or free money as many financial folks call it, a horrible work-sponsored retirement plan can really hurt your chances of saving enough for retirement. What’s the lesson here? Just because you have a 401(k) plan, don’t assume you’re better off by investing in it. And if you don’t have a 401(k) plan, don’t worry about it too much.

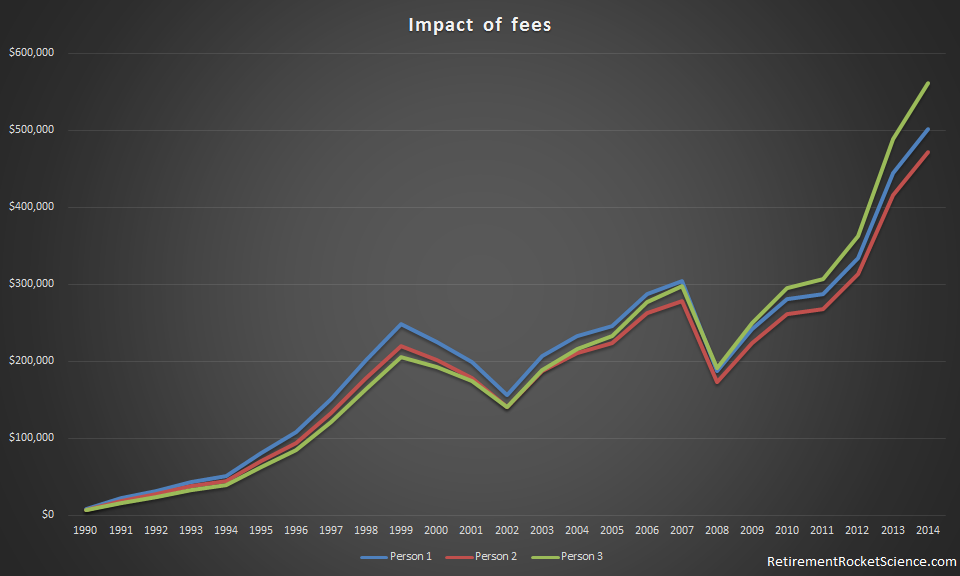

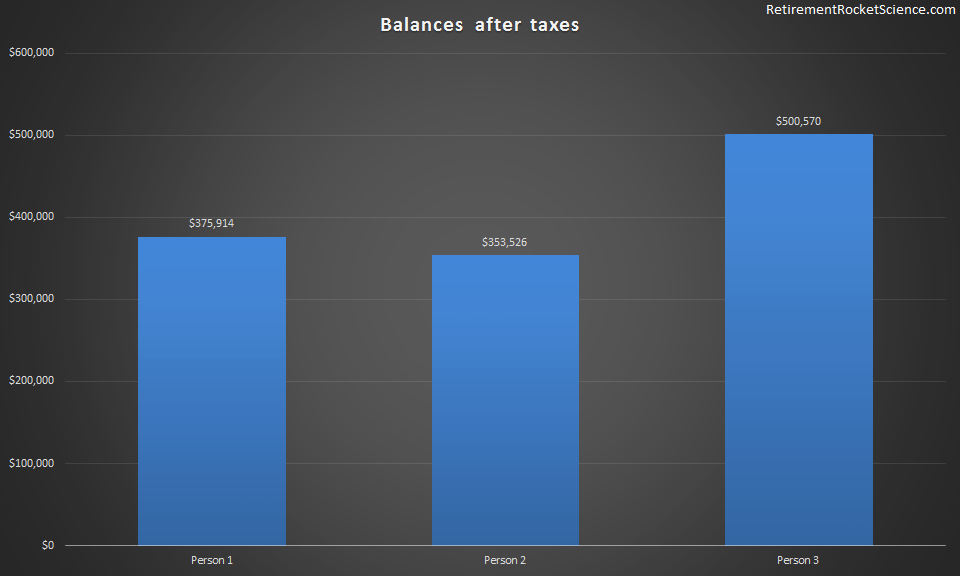

Here are the two charts again, but with folks saving 15% of their salary, and person 3 putting money into a brokerage account (step 4) instead of a Roth IRA (meaning they’ll pay taxes on their capital gains).

As you can see, how you invest if you don’t have access to a 401(k) isn’t really the right question to ask. No matter what options you have available, it’s important to make sure you’re investing in the best option for you based on the available information you have. The advice is the same for folks with a company sponsored plan and those without; watch fees, and think about the impact of taxes both today, and in the future.

If you have any questions or comments, you can reach out below or continue the discussion in the forum. If you are interested in receiving a notification of new posts, you can subscribe here.