Many years ago I was listening to a coworker talk about Christmas with his son, and he explained that his kid received so many presents that the family had to take breaks while he was opening them because he was getting overwhelmed. This fascinated me; his son got so many gifts from his parents and relatives that he wasn’t even enjoying Christmas morning. To top it all off, like most toddlers, after everything was opened, he had more fun with the wrapping paper, bows, and boxes than he was with the actual gifts.

Why do we do this?

I read a story about a potential Lego shortage in Europe around Christmas because the company can’t keep up with demand, to which one parent suggested the company come over to her house and take back all the pieces she’s been stepping on! For a toy that’s supposed to let a child use their imagination to build anything, people sure do spend a lot of money buying these highly customized sets.

The fact is, we buy our children a lot of crap they definitely don’t need, and in many cases, probably don’t even want. Think back to your own childhood, and can you remember more than 10 gifts you were given that meant a lot to you? 20? Now, how many bad gifts do you remember?

So what’s the fix for a family and friends that want to get a meaningful gift for a kid, or anyone else for that matter? How about a gift that will drive home the importance of saving early and often?

I know, I know, I can see the eyes rolling now. What kid wants an investment for a birthday or holiday? This is where you have the responsibility to rise above all of the messages of consumerism and start teaching small lessons on personal finance. I don’t think it’s any secret that schools aren’t doing a good job of teaching our youth this, and many parents don’t have the skills to do it either.

Since you’re reading this, chances are you can plant the seed early about saving for the future. Imagine giving a child an investment worth $100 as a gift when he or she is born. At age 24, when the now adult enters the workforce, that $100 might have grown into $542.74. $100 given every year until age 18 could be worth $6,000 at age 24.

What’s more amazing is the single gift of $100 could be worth $10,000 at age 67, and the gifts of $100 given each year until age 18 worth $110,000.

Statistics on how much we spend on kids around the holidays are hard to find, and I’m not sure how useful averages would be anyway. Still, I saw that the average adult spends $750 a year on gifts, while the average parent spends around $250 for each child. Why the disparity?

I’d guess some of this includes gifts for multiple kids, coworkers, significant others, aunts, uncles, grandparents, nieces, nephews, and grandkids. It’s those last 3 groups that are the focus here. The average kid probably gets enough presents at Christmas time, and probably has enough crap even if he or she didn’t!

So what are the arguments against giving an investment to a kid?

- You don’t want to seem uncool

- You might not understand how to give an investment

- You don’t want to create more work for the parents

I can’t help you with the first one, except to say one of my favorite aunts was one who had a small supply of inexpensive Mentos and Jolly Ranchers around when she visited. You’re not going to buy a child’s affection, so if you spend a lot of money around Christmas to try, just know you’re not going to succeed. You might make the child happy today, but not in the long-term.

If you want to give an investment, it’s possible to do so. Money Under 30 has an overview of giving stocks, mutual funds, and Treasuries. However, what would be ideal is a gift card that purchased $50 or $100 of an index fund like the Vanguard S&P 500 ETF (VOO).

Wish no more!

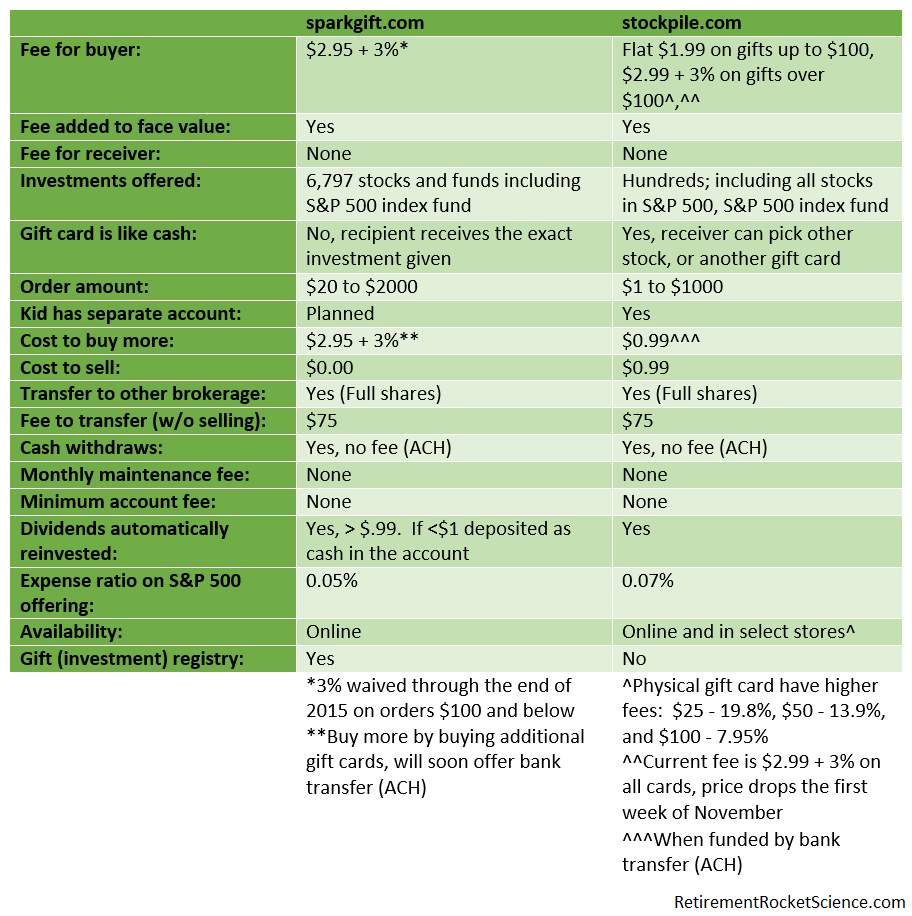

Two companies, SparkGift and Stockpile, now offer the ability to easily give an investment in the form of a gift card. The following table shows the difference (and similarities) between the two sites.

Pricing between the two companies is competitive, especially through the end of 2015 on purchases of $100 or less, when the 3% commission is waived for those purchasing the gift cards from SparkGift. Stockpile announced it will remove the 3% permanently on purchases $100 and less, and I wouldn’t be surprised of SparkGift extends their promotion. I would guess the 3% fee is in place to cover the costs of credit card processing, and the higher fees of the physical gift cards from Stockpile is profit given to retailers for selling these gift cards.

What would be nice is if the services offered a way for users to purchase the cards by transferring money directly from a checking account, which should reduce the fees. Realistically though, most people probably won’t care about the $2 – $8 in fees they’ll pay to give $100, but that can be a significant amount of money on a $25 or $50 gift, around 4% – 14%, depending on how you give the gift. The cheapest way to give is to do it online (with both services), but it’s likely in-store sales of physical gift cards will be popular (only offered by Stockpile).

Clearly both companies are aware of the other and offer a similar service. Which one is better might depend on your point of view. SparkGift offers significantly more funds for folks to buy, but I don’t know if that’s really a huge deal since most people would be better off giving an index fund. SparkGift offers many Vanguard funds, which have a lower expense fee than the index funds offered by Stockpile (Stockpile also has some Vanguard funds, but not as many). Stockpile also has an iOS app available.

Stockpile offers a more mature platform, allowing kids to have an account that is linked to a parental account. SparkGift plans on offering this ability soon. Where Stockpile really shines is in the ability for kids (or parents) to invest more money at only 99 cents a trade. To add more money to a SparkGift account you need to buy more gift cards, paying the fees mentioned above. Again, SparkGift intends to offer this feature in the future.

So what’s probably the biggest difference between the two? Stockpile allows the recipient to ultimately decide what happens to the gift. If you give someone $100 worth of Google stock, they can turn around and invest it in Microsoft, or cash it in for a $100 gift card to Best Buy. In a way, the Stockpile gift card is like cash.

SparkGift doesn’t allow this, and for that reason I prefer their service. If you give $50 of Vanguard’s S&P 500 fund, that’s exactly what the recipient gets. In a way, this forces the parents to make sure the custodial account is opened for the kid. At the very least, Stockpile should allow the giver to specify if the recipient has to buy the stock or fund specified. Of course, there’s a downside to this too. If the giver gives a “bad” stock, the parent can’t as easily pick a more prudent fund. Others may prefer Stockpile since the receiver of the gift ultimately has control over what they initially invest in. SparkGift allows for the creation of a registry, so you can register a newborn for a $200 index fund instead of a baby stroller.

So how do these services work?

For both services, you can go online, create an account, and enter the recipient’s name, the investment you want to buy, and the dollar amount. Stockpile asks for a bit more information when you confirm your email address. Then you provide the recipient’s email address and your payment information. That’s it! I don’t think either service could make it any easier. As previously mentioned, Stockpile also allows you to pick up a gift card at certain retailers too, bypassing the need for the gift giver to do anything online, though as mentioned in the chart above, the overall fee is higher if you buy it at a retail location.

The recipient (if not a minor) then goes to the site, enters some personal info, and claims the gift. When a minor gets a gift, it’s up to the parent to log into either site and set up a custodial account. Both companies make this exceedingly simple. A custodial account is a type of brokerage account that allows a parent to invest on the behalf of the minor. These accounts are also known as Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) accounts.

There are limits to how much money a person can give as a gift to another person without tax consequences (currently $14,000 a year). The other issue is taxes on interest, dividends, and capital gains. Children may earn interest, dividends, and capital gains (for example, if shares are sold for a higher amount than the purchase price) in their custodial accounts, whether or not they have to pay taxes depends on the amount in question.

In 2015, children do not have to pay tax on any of these earnings up to $1,050. For the record, that’s a huge amount of earnings. In 2014, the average return from dividends of the S&P 500 was 2.26%. A child would have had to have over $46,000 invested before any taxes would even be due.

In 2015, children do not have to pay tax on any of these earnings up to $1,050. For the record, that’s a huge amount of earnings. In 2014, the average return from dividends of the S&P 500 was 2.26%. A child would have had to have over $46,000 invested before any taxes would even be due.

The child does have to pay taxes on the next $1,050 in investment earnings, but at the child’s tax rate. If the custodial account has earnings exceeding $2,100, special tax treatment will be required so that the gains are included on the parent’s return. For the typical account I doubt this would ever be an issue, at least not while the child is still a child.

Other services like this have come and gone, but none of them had the low fees, ease of use, and variety of funds to invest in. I hope they both stick around, as they’re a great way to give investments to others, especially kids, to get them started on the path to financial freedom.

These sites are many times better than companies that allow you to give a framed share of a stock as a gift, often at a 100% or more markup. As the sites mature, it’ll be great for them to add resources directed at kids to help explain how investing works, so that by the time they enter the job market, setting up a 401(k) doesn’t seem like rocket science.

Gift cards make up a huge amount of holiday spending, with the average consumer spending $163 a year on them. In 2013, a staggering $118 billion was spent on gift cards, and yet an estimated $44 billion in gift cards has not been redeemed from 2008 to 2013. Instead of purchasing another iTunes or Starbucks gift card for someone, how about something a little more practical?

The next time you’re considering buying a gift for someone who has everything, young or old, consider giving an investment from one of these two sites. It’s something different, something useful, won’t collect dust, won’t be thrown away, and if forgotten about, will only become more valuable. It might not make you the most popular gift giver today, but imagine how much better the world would be if people spent a little less on gifts of consumption and gave gifts of saving and investing.

If you have any questions or comments, you can reach out below or continue the discussion in the forum. If you are interested in receiving a notification of new posts, you can subscribe here.