When it comes to reaching retirement age, a lot of folks are in denial that they’ll ever make it to this milestone, or they think that they’ll be able to get by without having any money set aside.

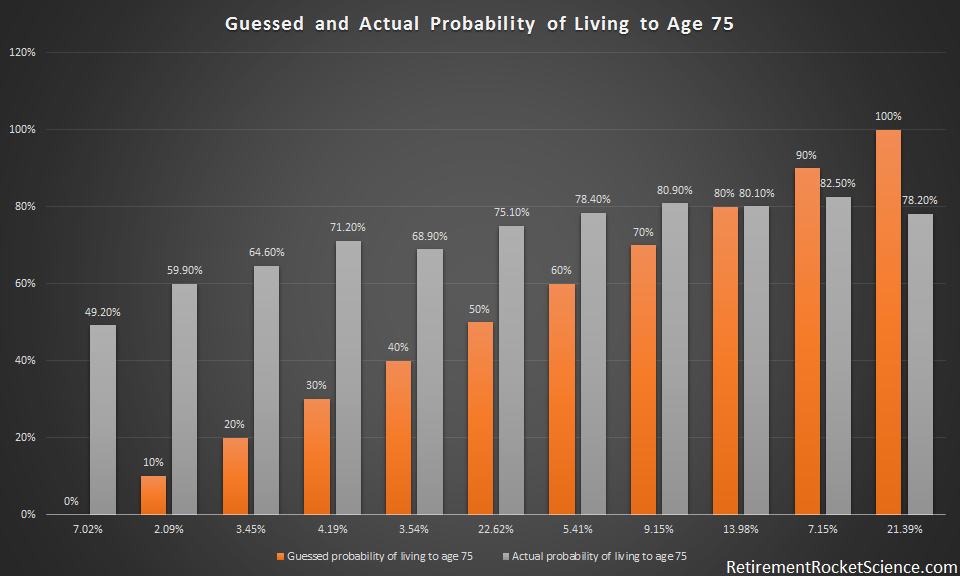

It turns out most people think they’ll live much shorter than they actually will. In 1992 the University of Michigan asked 26,000 people between the ages of 51 and 62 if they expected to make it to age 75. Folks who said they had a 0% chance of living that long were a little wrong; they had a 49.2% chance of making it to 75! Over 7% of folks surveyed said there was no chance they would make it to 75. 57.5% of respondents underestimated the probability of living to 75, while only 28.5% overestimated.

The chart below shows the percentage of people who said they had anywhere from a 0% to a 100% chance of living to age 75, along with the actual probability for each group. The only people who got it right were 13.98% of the folks who said they had an 80% chance of living to age 75; 80% of them actually did.

If you’re basing your retirement savings on your perceived time here on Earth, just be aware that almost 60% of people get it wrong. It’s much better to err on the side of caution. There’s an odd side effect of doing this too; people who expect to live longer typically do.

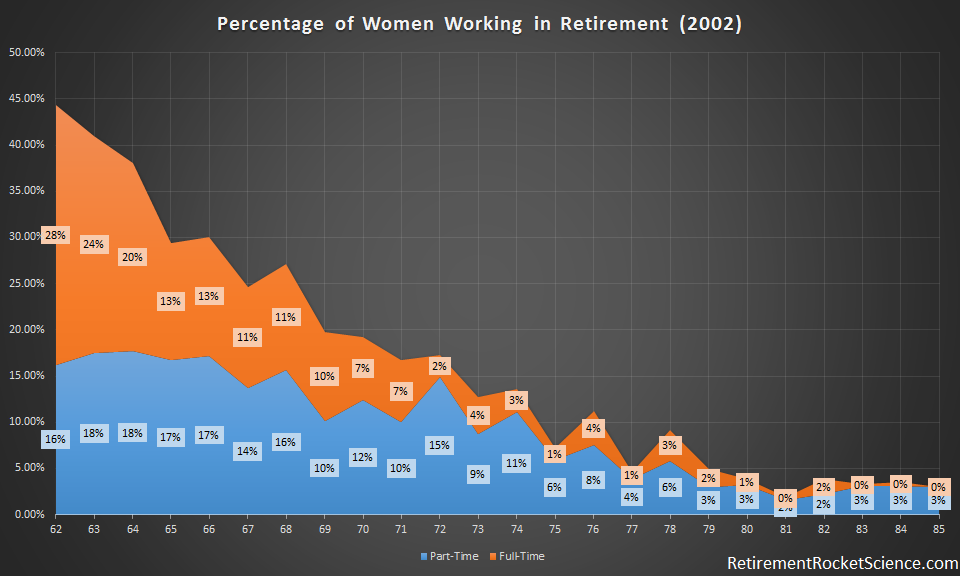

We already know the older you live, the longer you’re likely to live. If you don’t have a money set aside for retirement and think you can continue working, know that in 2002, less than 28% of men age 70 were employed, and less than 20% of women age 70 were, and for those that were, most work on a part-time basis.

The following charts show the are stacked, meaning the total number of people employed full-time is on top of the total number of people employed part-time. The individual breakdowns are provided for both full-time and part-time workers at each age from 62 to 85.

It’s one thing to joke about being a greeter at Walmart when you hit your golden years, but realize an average of 80% of the population doesn’t work at all past age 80. If you’re one of the lucky 20% that does work, you can look forward to a $7 to $9 salary if you take a job as a greeter, just remember, those living to 80 have a 50% chance of making it to 90.

It’s unlikely that the 80% group of non-workers have all of their finances in order, as around 64% of those age 55-64 have saved 1 year of their salary, while half of that group has saved nothing. But the real danger is basing your retirement strategy on death.

How do people do this? By not saving anything for retirement and assuming you will die before retirement, or that you or your spouse will die before retirement and maybe you can fund your retirement from an insurance policy. Insurance policies aren’t cheap. A 65 year old couple in good health could expect to pay $2,543.59 a month (or $30,523.08 a year) for $500,000 in coverage on a whole life policy, or $1,030.55 a month (or $12,366.60 a year) on a 20 year term life policy. If you smoke or have other health issues like obesity, you can expect those rates to climb to $47,616.84 a year for the whole life polices, and $42,129 a year for the term life. I’d imagine if most folks could afford those payments they could have afforded to set money aside for retirement each month.

What’s the moral here? If you remember The Matrix, Agent Smith said: “Do you hear that, Mr. Anderson? That is the sound of inevitability. That is the sound of your death.” We’ll all die, but just like Neo, probably a lot later than anyone thinks. Don’t plan your retirement thinking you won’t live to see your golden years, as this only does two things. The first is you statistically will die sooner, but most importantly, you won’t die anywhere near as soon as you think. Make a few modifications early on in your life, and you can save enough to be part of the 80% that not only doesn’t work past age 80, but doesn’t need to

What’s the moral here? If you remember The Matrix, Agent Smith said: “Do you hear that, Mr. Anderson? That is the sound of inevitability. That is the sound of your death.” We’ll all die, but just like Neo, probably a lot later than anyone thinks. Don’t plan your retirement thinking you won’t live to see your golden years, as this only does two things. The first is you statistically will die sooner, but most importantly, you won’t die anywhere near as soon as you think. Make a few modifications early on in your life, and you can save enough to be part of the 80% that not only doesn’t work past age 80, but doesn’t need to

If you have any questions or comments, you can reach out below or continue the discussion in the forum. If you are interested in receiving a notification of new posts, you can subscribe here.