If you need to take out a loan, borrowing from your 401(k) might seem like a good idea. Before deciding if you should, you probably need to think about why you want a loan in the first place. If you need to take out a loan for anything, it’s probably a pretty good sign that you can’t afford to buy what you want.

But just because you can’t afford something doesn’t mean you shouldn’t spend money to acquire it. Few people can afford a college education or a house, but if you’re wise about what you buy, you can come out ahead by borrowing money to pay for both.

That dream vacation on the other hand? Probably not a good use of any money if you might need to borrow funds for other expenses. Your kid’s college education? Not a good use of your retirement funds.

So what are the reasons people take loans out from a 401(k)?

So what are the reasons people take loans out from a 401(k)?

- There’s no approval required

- No application fee

- The interest you pay is paid to yourself

- No credit check

- They don’t imagine themselves retired

Why that last point? To be fair, it’s better to invest too much and realize you need to withdraw some of that money than to let your money sit idly by in a savings account earning next to nothing. But what about risk, you might ask? What if you invest $1,000 and the market tanks and it’s only worth $500, and you need that $1,000? If you’re cutting things this closely, it is worth taking a look at your budget and seeing if you have enough money set aside for unpredictable events.

You shouldn’t ever look at your 401(k) balance and think of the possibilities you have if you borrowed some of the money. If you wouldn’t take out some other type of loan to pay for the expense, you shouldn’t take the money out of your retirement account.

Surprisingly though, a lot is misunderstood when it comes to 401(k) loans. Let’s imagine you take out a $10,000 loan. Your company charges an interest rate of 1.5% plus the prime rate, which is currently 3.25%, for a total of 4.75%. Most companies charge prime plus 1% to 2% (4.25% to 5.25% total as of 11/2015). You typically have 5 years to pay the loan back. At a 4.75% interest rate, this means you’d have 60 payments of $187.57. You would pay a total of $11,254.20, with $1,154 or about 11%, being interest.

A lot of people say you it’s okay to pay the interest because you’re paying it to yourself, instead of a bank. In that way, it’s a sort of forced savings. Each month you’d be investing an extra $20.90 from the interest that you’d otherwise be paying to whatever financial institution offered you a loan.

I’ve heard from many people who think 401(k) loans are a bad idea because you’re withdrawing tax-free money and repaying it with money you paid taxes on. While 401(k) loans may be a bad idea, this isn’t a reason why. This is because no matter what type of loan you took out, you’d be paying the money back with post-tax money.

The reason for so many differing opinions is because people confuse the message. The first question is, do you actually need a loan. The second question is, if I need a loan, is a 401(k) loan a smart choice?

Why is it so hard to get yes or no answer to this last question? In general, it’s because you need a crystal ball to answer it. But if we violate one of the cardinal rules of investing, and base future returns on past performance, a 401(k) loan is typically a horrible decision. Here’s why.

The money you save in your 401(k) should be invested for the long term. Depending on how many years you have until you retire, it’s not unrealistic to invest 100% of your money in a S&P 500 index fund. Over any 30 year period since the S&P 500 existed, the average return was 11.17%, with the lowest being 8.11%. Based on that average, every year your money was out of your 401(k), you’d be losing out on that growth.

Even though the lowest return over a 30 year period was 8.11%, since I use 7% on all of my calculations, I’ll continue with that. Let’s imagine you have a $100,000 401(k) balance, make $50,000 a year, and save 6% of your salary, while getting a 3% company match. We’ll assume you take out a $10,000 loan at 4.75% interest, and pay it back over 5 years.

For plan B, we’ll assume you take a personal loan for $10,000 at a 7.49% interest rate for 5 years.

If you own a home, you might be able to take plan C, where you take out a home equity loan for $10,000 at a 4.63% interest rate for 5 years.

The hardest thing about doing these comparisons is there isn’t a common frame of reference. If you take out a loan, you have to pay it back, and that money has to come from somewhere. If you don’t take out a loan, you have no money to pay back, but it’s hard to say you actually saved anything. After all, I can’t say I saved $10,000,000 by not going to the moon last weekend.

So to make all of these comparisons equal, we’ll assume your budget has $200.33 a month that you can either additionally contribute to your 401(k), or use to pay off any sort of loan. Now we have a common frame of reference.

So what would your account balance look like after 5 years under these scenarios?

Clearly not taking out a loan puts you in a better place, but you can see the 401(k) loan is the middle option if your alternative is a high-interest loan.

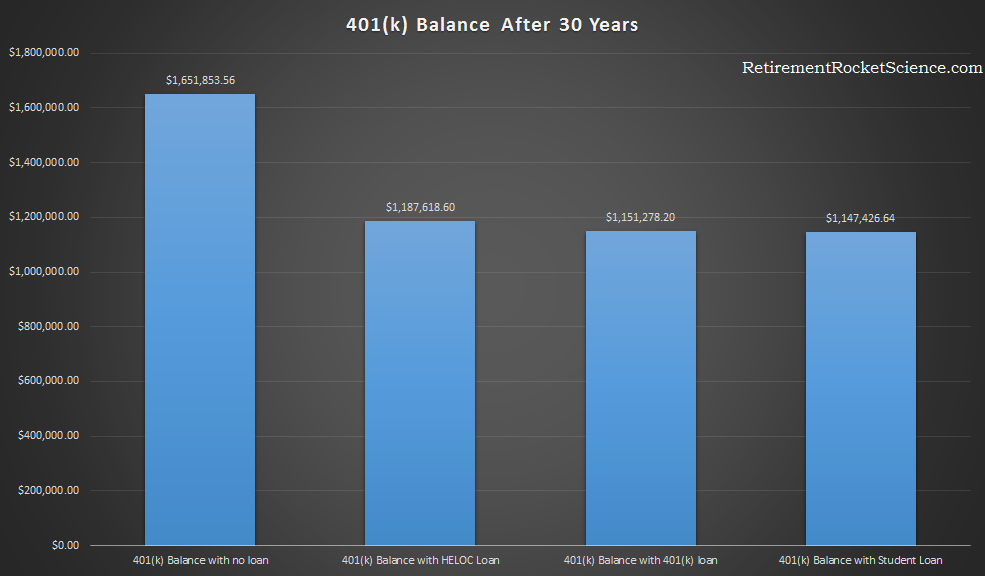

Assuming you continued to invest for 25 more years, here’s what your final retirement balance would look like under the four scenarios.

As you can see, the longer you have until retirement, the more your 401(k) balance will be affected by taking a loan from it.

To take this to the extreme, we’ll imagine someone needs $50,000 of his or her $100,000 balance. They plan to repay it over 10 years. If they have a house, borrowing against home equity might be a possibility. Currently, you can get a $50,000 home equity loan with a 4.04% interest rate for 10 years, which would have a monthly payment of $507.18.

It would be very difficult for someone to get a $50,000 loan without any collateral, but we’ll assume someone is considering financing grad school with a 401(k) loan instead of a graduate student loan, which currently have a rate of 5.84%, or a payment of $551.09 a month for 10 years.

We’ll use $551.09 as the number that can either be invested in the 401(k), or used to pay back the loan, or a combination of both. Why include the option of not taking out a loan and instead investing that money? For some, it might make them reconsider if that addition or new kitchen is really necessary.

So what do things look like 10 years later?

And 20 years after that?

Remember that part about the crystal ball though? The average return over all 30 year periods the S&P 500 existed was 11.17%. Here’s what those charts look like using this average return.

After 10 years:

After 30 years:

The lesson is, the better the market performs, the worse of a deal a 401(k) loan is. On the flip side, if you took out a 401(k) loan at the peak of the market in 2007/2008, and paid it back after the market crashed ~50%, you would be telling anyone who would listen about the money you didn’t lose in the market. But don’t forget, if you were one of the millions who lost their job, you might have been scrambling to find a way to pay back the loan.

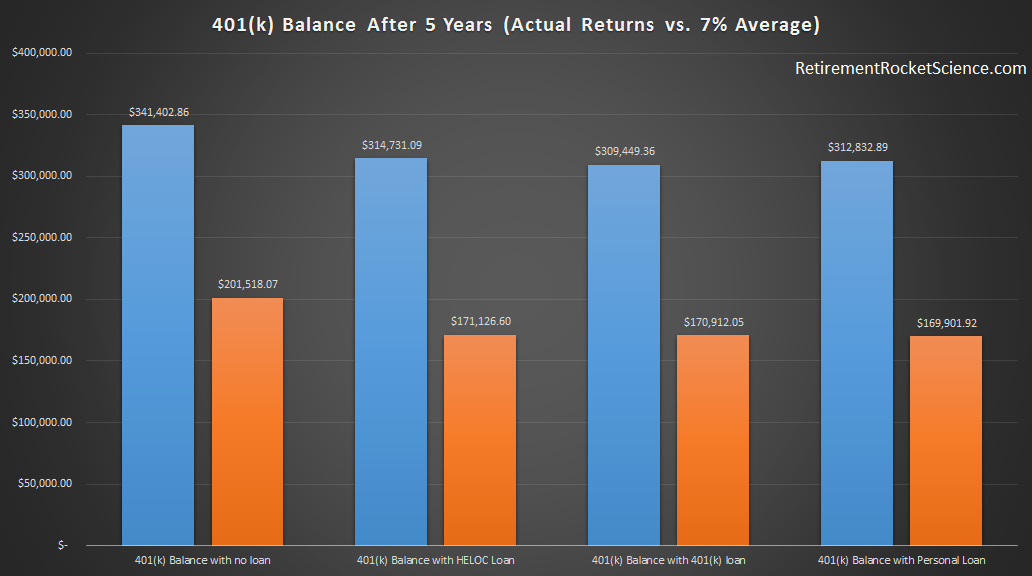

It’s possible to think charts based on actual market returns, instead of average market returns, would be more helpful at illustrating these concepts. In reality, they wouldn’t be very useful. We have no way of knowing if those returns, or the patterns of those returns, are going to occur in the future. Since folks investing for retirement are in it for the long haul, time is on their side.

But just because we shouldn’t doesn’t mean we won’t! It’s actually interesting to apply historical returns and re-run the simulations. Here is the data from the first chart in this article (orange), compared with the actual S&P 500 return (blue) from 1985 to 1990 for the 5-year loan.

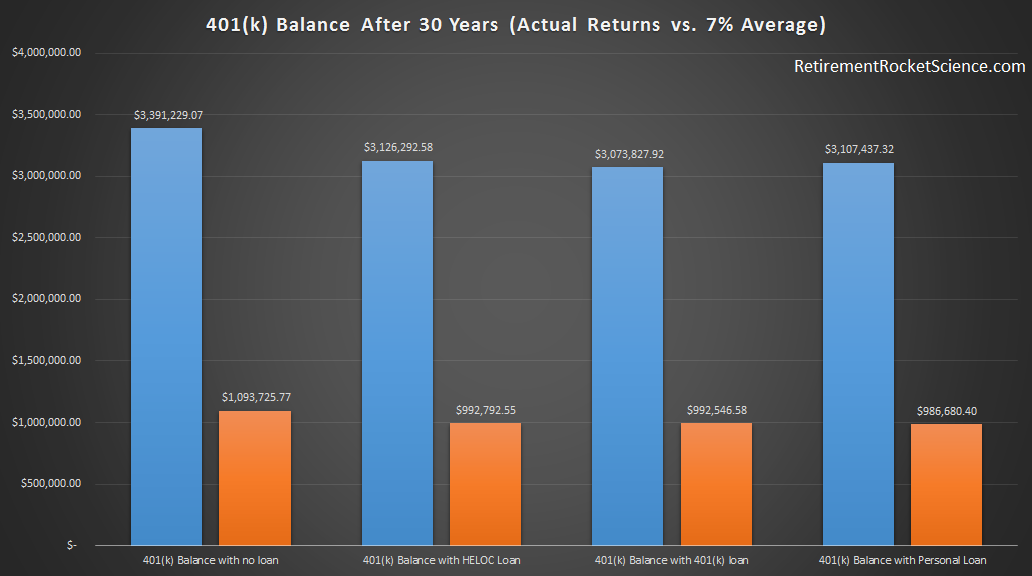

Here is the ending balance with the actual returns (blue) from 1985 to 2014 (30 years).

As you can see, in all situations, taking a 401(k) loan provides you with the lowest 401(k) balance out of all the other options.

So when is a 401(k) loan a really bad idea?

- When you have other options available to borrow money

- If you don’t feel your job is secure

- You think the market can only go up

- You don’t really need the money

When is a 401(k) loan a not really bad idea?

- You have no collateral

- Your other options have sky-high interest rates

- You have no other options

- You feel pretty secure about your job

- You’ll pay the loan back very quickly

In a way, employers make it too easy to access retirement funds. Sure, it’s your money, but it’s also you’re retirement, and no one wants to set you up for failure.

If you have any questions or comments, you can reach out below or continue the discussion in the forum. If you are interested in receiving a notification of new posts, you can subscribe here.