Deciding which college to go to is a big decision, and one of the biggest financial decisions you’ll make. Until you buy a house, then that will be the biggest financial decision you make. Unless you have kids, then they’ll be the biggest drain on your finances, probably in part by their choice on where to go to college!

We’ve seen gas prices and housing prices on a roller coaster over the past decade, but like health care expenses, college tuition has only been going up. And just like health care, a lot of people think you get what you pay for.

We’ve seen gas prices and housing prices on a roller coaster over the past decade, but like health care expenses, college tuition has only been going up. And just like health care, a lot of people think you get what you pay for.

People often think if something is more expensive, it’s better, but when it comes to education, it’s wise to ask: better how?

Students learn more information? A better city to live in? Better campus housing? Newer technology? Higher rated faculty? Better graduation rate? Better selection of majors?

In 2000, a Department of Education study found that there actually is a positive relationship between wages and attending a highly ranked university. Men who attended a university that was one standard deviation higher on quality measures saw their salaries jump 8.1%. Women who did the same saw a 17.4% increase. The author calculated the increase could translate to an extra $107,000 for men over the course of a lifetime, and $173,000 for women.

That might sound like a lot of money, but there are a couple of catches. First, we assume a top-tier university has a sticker price of $60,000 a year ($240,000 for 4 years), a state school runs $19,000 a year ($76,000 over 4 years), while the average private university is $42,500 ($170,000 for 4 years).

The next thing to consider is financial aid, and that’s a lot harder to estimate. If you (or your kid) is bright, there are most certainly scholarships available. If your family doesn’t make a lot of money, there are additional grants and scholarships available. The Department of Education provides some averages, with students from higher income families attending a public school getting an average of $1,680 a year in scholarships, and private school students getting $13,220.

It’s important to note that someone who might get a full scholarship to top 50-100 school might get next to nothing to attend a top 10 school. We’ll ignore this though, and assume over 4 years the public university costs $69,280, the average private university costs $117,120, and an elite school runs $187,120, all after scholarship awards.

Now it’s time for a little math. Assuming each student above pays for their 4 years of school with student loans, for the next 10 years the public school graduate would pay $711 a month on their loans, the average private school graduate would pay $1,203 a month, and the top-tier student would pay $1,921 a month.

That amount of cash would be hard for most new graduates to come up each year; $8,532, $14,436, and $23,052 a year. The private and top-tier graduates might need a longer repayment schedule, but we’ll assume they live on Ramen for 10 more years.

The average college graduate earned $45,327 in 2014. The Department of Education report found that on average, the attributes of a college contributed to 2% to 3% of income for men, and 4% to 6% for women. We’ll assume private school graduates earn 3% more if they’re male, and 6% more if they’re female, than their public school peers.

Unfortunately, on average women earn 79% of what men earn, and so we’ll assume a starting salary of $35,808. With that salary, it would be difficult to pay back the student loans in 10 years.

After working from age 23 to 67, with annual 3% raises, the male private school graduate would have an ending salary of $166,415.91, the private school graduate would make $176,400.87, and the top-tier graduate would make $195,372.29.

The female public school graduate would have an ending salary of $131,467.36, the private school graduate would make $139,355.40, and the top-tier graduate would make $154,342.68.

Their earnings over their lifetime are even more dramatic:

Sounds great, right? Go to a highly ranked school, earn more money! I hope you didn’t forget about those student loans.

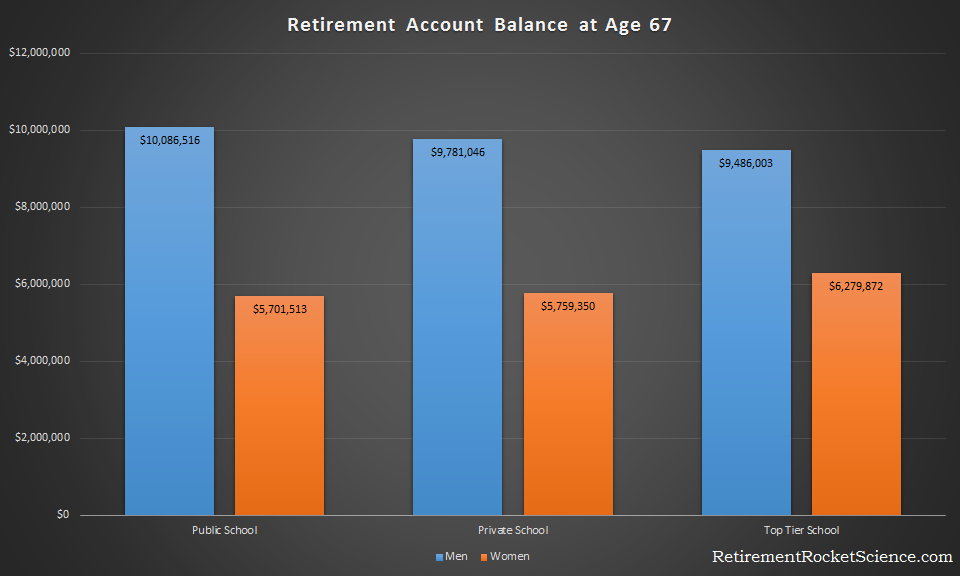

To show the impact of student loans, we’ll assume every graduate sets aside the same base amount every month towards paying back student loans and funding their retirement accounts: $1,921. This number just happens to be the amount of money the top-tier university graduate would have to pay each month towards student loans. We’ll also assume that the private school graduate and the top-tier graduate save the additional money they make each year from the higher salaries they earn as a result of attending “better” schools.

So what will those retirement balances look like at age 67, assuming the usual 7% annual return?

Were you surprised?

The men clearly make out by being able to invest more money early in their careers instead of using that money to pay down student loans. So why does it look like the women are better off?

The reason is because earlier we said each person sets aside $1,921 plus the difference in their salary to invest. This means the women are investing the same amount (or more) than the men, but will have much less income left over each month. For public school graduates, this means that while the women invest the same amount as the men, they would have $793.25 less each month in spending money. This next chart shows how much money each person would have to live on each year after investing and paying off student loans.

As you can see, the wage gap is huge. Since it’s not possible to equalize the playing field by increasing the wages of the women, we’ll do it by taking away money from the men. If both men and women have the same amount of money left over each month after investing and paying off student loan debt, here’s what the final retirement balances look like. To get this chart we take away money from the men until they are living off of the same amount as the women, and put that money towards retirement.

This last chart should really drive home the importance of finding a good paying job early in your career. If you’re not making at least the average for your industry, you should spend a little time each week trying to find ways to get there. It should also highlight the importance of encouraging women to study fields with higher incomes.

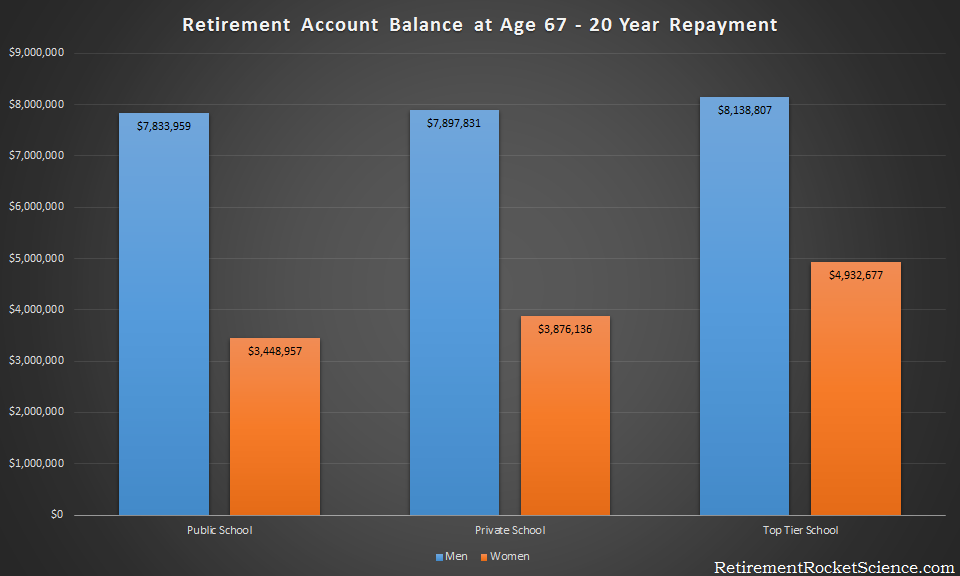

My only complaint with these charts is I don’t believe the average person is willing to put such high amounts of money towards student loan debt and investing each month. With a 20-year repayment plan, assuming the loans have a 4.29% interest rate, the monthly payments would be $430.49 for the public school graduate, $727.75 for the private school graduate, and $1,162.71 for the top-tier graduate.

Here’s what the final retirement balances look like assuming a 20-year payback.

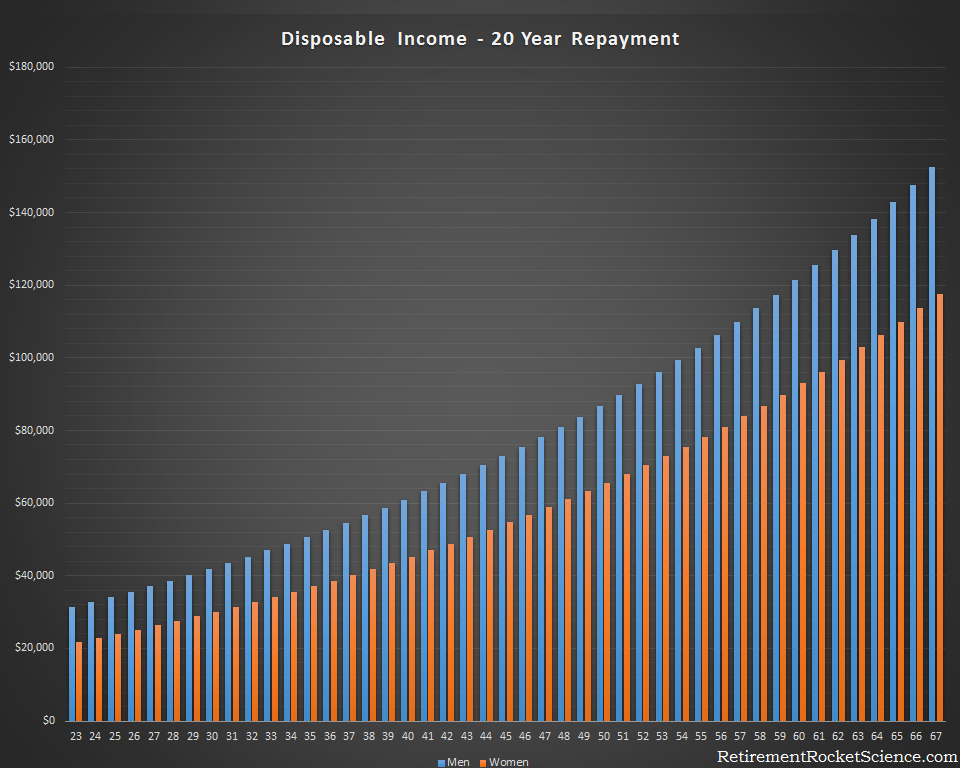

Here’s a chart showing the increase in what’s left from their paycheck as a result of less money is being applied to student loan payments and investing each month.

The difference between these two sets of charts is the amount invested and put towards loan payments decreases by $758.29 a month, which means more money in the graduate’s pockets, and less money in their retirement accounts. As you can see from the charts, there’s no free ride. Here’s how much the retirement balances decrease when extending the loan payments from 10 years to 20 years.

The interesting thing to note, is that while the story looks better for more expensive universities when you extend the loan payback time, the public university graduate could pay his or her loans off in 10 years with a monthly payment of $711, and thereby have a much higher balance at retirement, while the private university graduate would pay $727.75 a month over 20 years, and have millions less at age 67. The top-tier grad would pay $1,162.71, also over 20 years.

The rub is, these charts don’t tell the whole story. Some research shows it’s not which college you attend that determines your future income, but which colleges you apply to. Smart people are typically successful regardless of where they go to school, or if they go to school at all. And if that’s the case, why attend a school that’s going to cause financial stress?

What the charts do show just how detrimental student loan debt is towards saving for retirement, a house, and having children. Think carefully about the college you decide to go to. The prestigious name might look good on the diploma, but that won’t matter much come retirement.

If you have any questions or comments, you can reach out below or continue the discussion in the forum. If you are interested in receiving a notification of new posts, you can subscribe here.