Whenever families get together, there are inevitably thoughts about topics that no one should bring up. Don’t mention religion, avoid topics about money, and whatever you do, don’t bring up politics. I can’t help you with politics and religion, but when it comes to financial matters, it doesn’t make sense to keep quiet.

With any personal topic, the point here isn’t to gossip and judge. “You know, Uncle Mark would have been able to retire by now if the idiot didn’t invest everything in a single stock. I always knew Enron was a bad company.” The point is to inform. The world of personal finance and retirement planning change quickly, but the fundamentals remain the same.

So what kind of topics might come up, and what advice can you give?

“My company doesn’t offer a 401(k), should I start investing in a myRA?”

A myRA is great in that it makes it easy for people to set aside some money each month, up to $5,500 a year. To put things into perspective, an envelope is also a great way to set aside some money each month. What are the upsides to a myRA? It’s risk-free, and there are no fees to participate. What are the downsides? The return on your investment is low. If you’re young enough to be considering a myRA, you need some risk in your life.

A myRA is basically a Roth IRA administered by the Treasury instead of a company like Fidelity or Vanguard. The catch is there’s only one fund to invest in, the Government Securities Investment Fund. In the past 10 years, the average return on this fund has been 3.19%.

What’s a good alternative? Hardly anyone can go wrong with regular Roth IRA invested in a low-cost index fund, such as the S&P 500. It has returned 6.8% over the past 10 years.

When might a myRA be a good idea? If you don’t have the funds to open up a Roth IRA today. Some banks require a minimum deposit amount to open a Roth IRA (Vanguard’s minimum is $1,000, while USAA only requires $250). If you have a myRA, once you get the minimum you need to open up a Roth IRA, you should move your money.

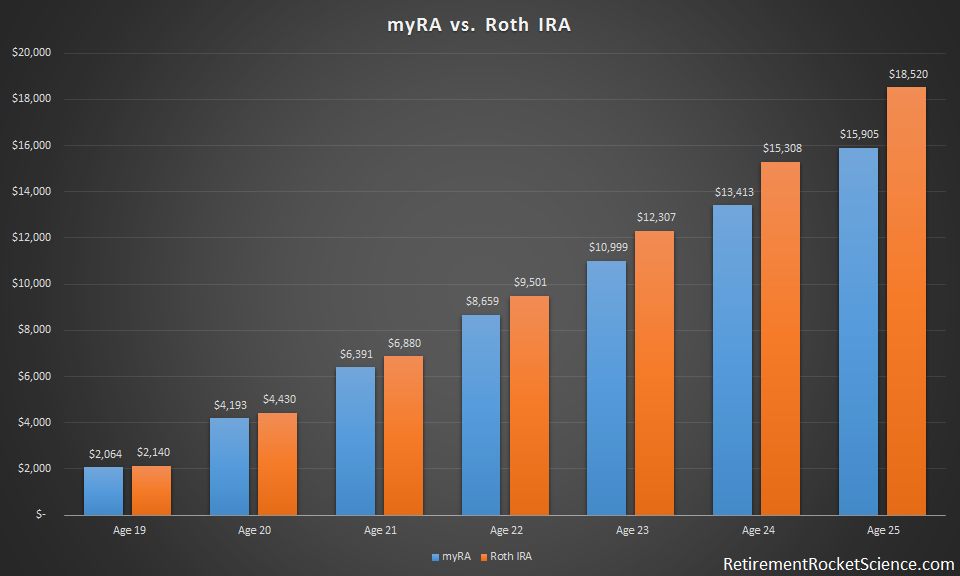

Let’s say someone can invest $2,000 a year starting at age 18 until age 25. Here’s what things would look like if they invested in a myRA versus an S&P 500 index fund (assuming the usual 7% annual return).

You might be thinking those differences aren’t that substantial. Here’s the next lesson you can drive home; the importance of saving even a little amount of money when you’re young. If at age 25 the myRA was moved into the same fund as the Roth IRA was invested in, and no additional money was invested, here’s how each one would grow.

At age 67, the account started in a myRA would have $272,680, and the Roth IRA account would have $317,505. That’s a difference of $44,825, or a 16.44% higher balance by starting off with a Roth IRA.

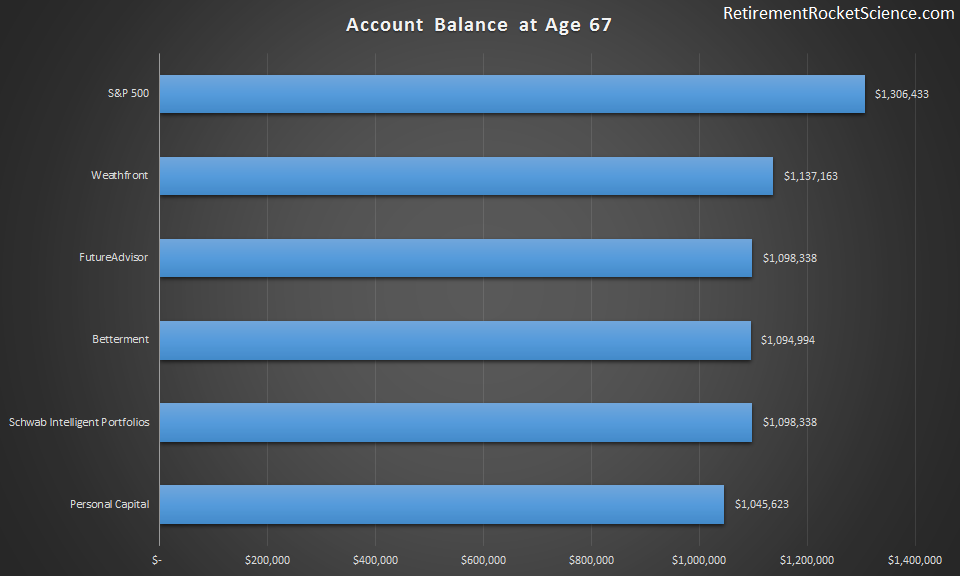

“I just heard about Betterment / FutureAdvisor / Schwab Intelligent Portfolios / Personal Capital / Wealthfront, should I move my money there? I heard the fees are lower than using an advisor.”

It’s true, the fees of robo advisors are lower than the fees charged by human advisors. The first question you should ask is if you need any advisor. Most folks are better not trying to beat the market, and instead investing in low-cost index funds. There are a lot of great sites comparing the fees of these different services. It’s not easy to compare them because some fees differ based on the total amount you have invested, while others force you to invest in certain funds, which have higher fees than available alternatives.

Based on the fee information available, here’s how much money the typical investor could have after letting the companies above manage their money if they deposited $5,000 a year from age 25 to 67. If the companies have a minimum deposit amount, I assumed the money was saved in an index fund until the minimum was met, then it was transferred.

This chart isn’t exact, since there’s no way to actually know the return you’d get with each company. But it should really make you think about if you’d get ~$170,000 to $260,000 worth of value from a robo advisor. The important thing to realize is that over time, investors rarely beat the market. But even if they do, you have to wonder at what cost.

“What should we get the kids for Christmas?”

This one is easy. Take a look at sparkgift.com and stockpile.com. They both offer great ways to give kids (or anyone else for that matter) an investment. It beats giving junk that will sit around and collect dust.

The next time a money topic comes up, don’t shy away from it. Perhaps more people would be in a better place financially if they knew a little more about saving and investing. Perhaps they think it’s normal to not save anything because that’s the message their hear from the media. Share the link to this site to others to get them thinking about strategies for a secure retirement.

If you have any questions or comments, you can reach out below or continue the discussion in the forum. If you are interested in receiving a notification of new posts, you can subscribe here.