You might think the worst part about saving for retirement is the impact from having less spending money today. But typically after a while, you adjust to your current expendable income, and the pain goes away. The worst part is simply that it’s boring to save for retirement.

Why is that?

The reason it’s boring is because typically nothing exciting happens as your nest egg grows. Even after you manage to get a sizable amount saved, at a 7% return, watching your investments increase is like watching paint dry. If you have $1.5 million saved, and it grows 7% a year, your account balance would go up an average of $287 a day. $1,495,362.23 doesn’t look much different from $1,495,649.90.

When things do get exciting is when something spectacular happens, but those moments are exactly when you should keep a level head. Watching your investments go from $1,495,362.23 to $1,226,197.03 will probably get your attention. Instead of panicking when an account drops 18%, just realize you’re getting a discount on the investments you make today. Who wouldn’t mind an 18% off coupon? Extraordinary events don’t happen often, but you would have a hard time believing that if you pay attention to the news.

If you listen to or read the news related to investing, it’s usually short-term doom and gloom. Oil is down; the economy is going to collapse because all of the oil companies will fail! Oil is up; the economy is going to collapse because consumers can’t afford gas! Stocks are down because the Fed is going to raise interest rates. Stocks are down because the fed didn’t raise interest rates!

If you’re saving for the long haul, you’re better off tuning out all of this information. When I read stories about how this Christmas is going to be good or bad for businesses, I can’t help but think: who cares?

If you own stock in Amazon, and you hear this Christmas is going to be bad, should you sell it? If you hear it’s going to be good, should you buy? What if you invest in low-cost index funds, should you buy or sell then?

There is a lot of data available to actually find out of there’s any reason to listen to the fear-mongers of the world, but without even seeing a chart, I’m sure savvy retirement savers won’t be surprised at the results.

So why are there so many reports on the day-to-day movements of the economy? Because people pay attention to them, which means more ad revenue. Like an accident on the highway, most people have can’t help but to slow down and look. But just like an accident you stare at, if you pay too much attention to what’s going on in the other lane, instead of your own, you’re bound to wreck your own retirement.

How, you might ask?

If you start listening to people who just say anything without seriously considering the consequences or validity of what they say, you’ll slowly be influenced by them.

Maybe this isn’t a good time to increase my 401(k) contribution. Maybe the job market is worse than I thought so I should be thankful I have a job instead of looking at other opportunities available. It sounds like interest rates will stay low for a long time, so I’ll take out an adjustable rate mortgage.

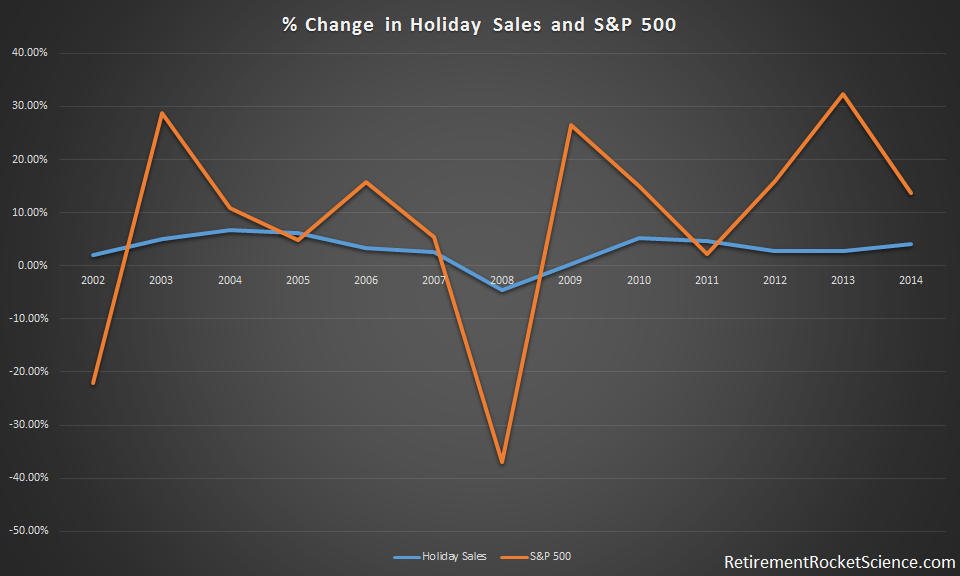

Take holiday sales as an example. Every year I hear that holiday sales are down, but from 2002 to 2014, there was only 1 year when holiday sales were lower than the previous year. What is actually down is the percent increase in sales from one year to the year before. I’m not sure what rational person would get a $1,000 raise one year, a $1,500 raise the next year, and a $1,600 raise the third year and then say that raises are down. Yes, you got a 50% higher raise the second year compared to the first, and only a 6.7% higher raise compared to the amount you got the third year. You wouldn’t honestly tell people that raises are down 43% would you? Makes you wonder why the media does.

Take holiday sales as an example. Every year I hear that holiday sales are down, but from 2002 to 2014, there was only 1 year when holiday sales were lower than the previous year. What is actually down is the percent increase in sales from one year to the year before. I’m not sure what rational person would get a $1,000 raise one year, a $1,500 raise the next year, and a $1,600 raise the third year and then say that raises are down. Yes, you got a 50% higher raise the second year compared to the first, and only a 6.7% higher raise compared to the amount you got the third year. You wouldn’t honestly tell people that raises are down 43% would you? Makes you wonder why the media does.

At any rate, here’s a graph of the change in holiday sales against the change in the S&P 500. If you can see a pattern in all that, you might have a future on a news network!

Also in the news is when the fed will raise rates. Sure it’s nice to get higher interest rates on low-risk investments, but most investors saving for retirement need exposure to stocks. So what does the change in the Fed Rate look like compared with the change in the S&P 500?

Again, you must have a pretty good imagination to find anything that looks close to a correlation. The last chart is the most interesting to me. You hear about the price of crude oil in the news every day. To me it’s like hearing about the weather, there’s nothing I can really do if it’s going to rain except to bring an umbrella. The best thing I can do to hedge against higher oil prices is buy a fuel-efficient car and make my home as energy-efficient as possible.

Here’s a chart of the change in gas prices over the years against the S&P 500.

This chart seems to have a little of everything. The change in the S&P 500 lagging the change in gas prices, then no discernible pattern, and finally the change in gas prices lagging the changes in the S&P 500. But again, humans are great at finding patterns where they don’t exist.

The moral of these three charts is to drive home how little the daily economic news should impact your investing decisions. We already know you can’t time the market, make sure you don’t get worked up about news you can’t do anything with.

If you have any questions or comments, you can reach out below or continue the discussion in the forum. If you are interested in receiving a notification of new posts, you can subscribe here.